Nicolet Wealth Management Monthly Newsletter - 10.2.24

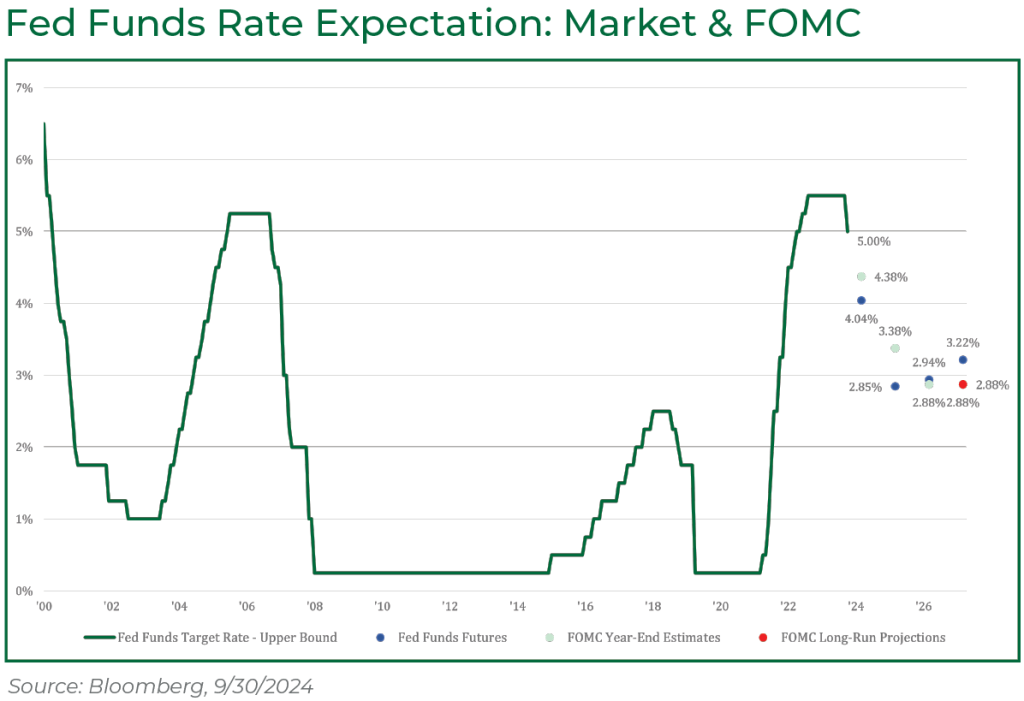

Fed Funds Rate Cut by 0.50%

In a somewhat surprising move, the Federal Reserve cut its target policy rate by 0.50% to a target range of 4.75% - 5.0%. Prior to the Fed’s September meeting, the chance for a 0.50% rate cut was about 60-70%. However, during the press conference following the announcement, Chair Jay Powell noted that nobody should assume that “this is the new pace” for reductions going forward. Projections were also updated, with a narrow majority of 10 out of 19 Fed officials favoring to lower the target policy rate by another 0.50% by the end of the year or a 0.25% rate cut over the next two meetings. Next year, policymakers see another 1% of rate cuts. On the economy, Fed chair Jay Powell said that had the Federal Reserve known of the weak July jobs report when they met at the end of that month, rate cuts would have happened at the last meeting. However, the Federal Reserve sees the economy as “basically fine” with the expectation of the job market avoiding a substantial rise in unemployment.

Lower Rates Boost Mortgage Applications

The refinancing index published by the Mortgage Bankers Association rose to the highest level since April 2022, as the contract rate on a 30-year fixed mortgage declined to 6.13% on its eighth straight weekly drop. A falling 30-year fixed mortgage rate has followed the market’s heightened expectations for a lower Federal Reserve target policy rate through the end of 2025. Despite a resurgence in refinancing, it remains depressed relative to 2020-2021 given that most homeowners still have historically low-rate mortgages. In addition to refinancing activity, home-purchase applications jumped to the highest level since early February and the fifth straight weekly advance. Solid economic activity, boosted by strong consumption, coupled with lower rates continues to be a positive backdrop for housing.

Treasuries Extend Multi-Month Rally

Following the highly anticipated Federal Reserve target policy rate cutting cycle in 2024, Treasuries of various maturities exhibited rate declines. The Bloomberg US Treasury Total Return Index returned 1.2% in September, extending its positive return streak to 5 straight months, making it the longest winning streak in 14 years. The 10-year Treasury yield declined 0.12% in September and 0.90% from the beginning of May to a level of 3.78%. The aggressive path of rate cuts going forward is the biggest risk for Treasuries through 2025 as any slowdown in cuts could weigh on Treasury performance.

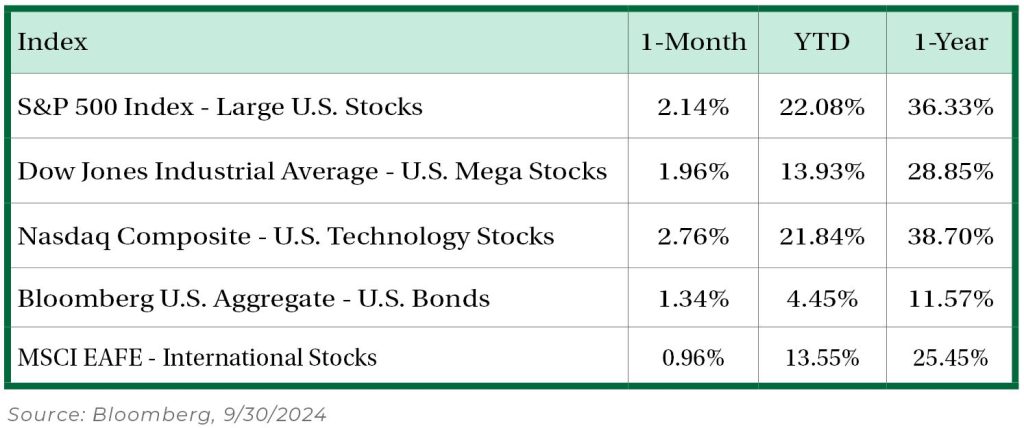

Emerging Markets Stocks Accelerate

Since global equity markets bottomed on August 5, emerging market stocks have exhibited a resurgence, leading all indexes in performance. The S&P 500 index (Large US companies) returned 11.4%, the MSCI EAFE (international developed stocks) increased 12.5%, and the MSCI Emerging Markets Index rose 15.7%. There are a few reasons for this change in the global equity landscape. The first is a weak dollar. The U.S. dollar index declined -1.8% since August 5. Stronger global currency is an indication of better growth prospects outside of the US. Secondly, two of the largest equity markets in the MSCI EM index have outperformed US stocks, particularly China. There’s been a noticeable change in China’s government to focus on growth policy following its most recent politburo meeting.

Investors Find Comfort with Growth Stocks

After multiple months of outperforming, value stocks took a backseat once again to the growth segment of the stock market. In July and August, investors became skeptical that growth stocks would be able to live up to their lofty earnings expectations after some unsettling economic data points. In September, the S&P 500 Growth index returned 2.8%, the S&P 500 index increased 2.1%, while the S&P 500 Value index advanced 1.1%. The technology sector contributed the most to returns, led by NVIDIA, Microsoft, and Broadcom, while Amazon and Tesla contributed to the consumer discretionary sector’s second-best return. Financials, Energy, and Healthcare had negative returns during the month despite financials contributing the most to returns in the third quarter.

Although we believe it to be reliable as of the publication date and have sought to take reasonable care in its preparation, all information provided is FOR INFORMATIONAL PURPOSES ONLY and we make no representations or warranties regarding its accuracy, reliability, or completeness and assume no duty to make any updates in the event of future changes. Past performance may not be indicative of future market results. Any examples used (including specific securities) are generic and meant for illustration purposes only and are not, and should not be interpreted as, offers to buy or sell such securities. To the extent indices are referenced, please note that you are not able to invest directly in an index.

Nicolet Wealth Management is a brand name that refers to Nicolet National Bank and certain of its departments and affiliates that provide investment advisory, trust, retirement plan level services, and insurance services. Investment advisory services offered through Nicolet Advisory Services, LLC (dba Nicolet Wealth Management), a registered investment advisor.

All investments are subject to risks, including possible loss of principal, and are: NOT FDIC INSURED; NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; AND NEITHER DEPOSITS OR OTHER OBLIGATIONS OF, NOR GUARANTEED BY, Nicolet National Bank or any of its affiliates. Neither Nicolet Advisory Services nor its affiliates offer tax or legal advice. You should consult with your legal and tax professionals before making investment decisions.

Listen & Subscribe to our Podcast

Tune in for the next episode, subscribe or follow us wherever you listen to podcasts.

Related Posts